Highlights from last week

CPI

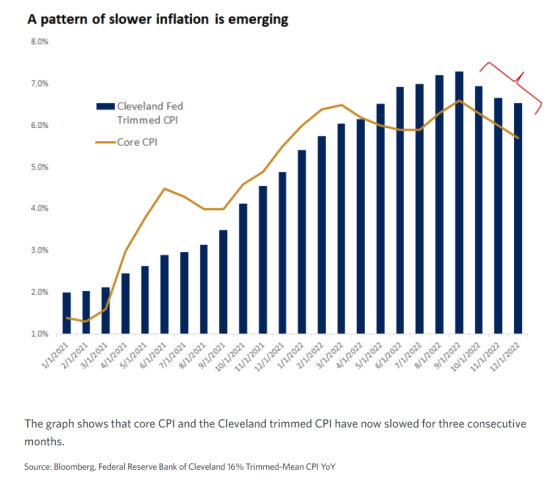

The consumer price index (CPI) decelerated further, with December marking the smallest annual increase since October 2021. Paired with the November and October data, core inflation (which excludes the volatile categories of food and energy) has now slowed for three consecutive months.

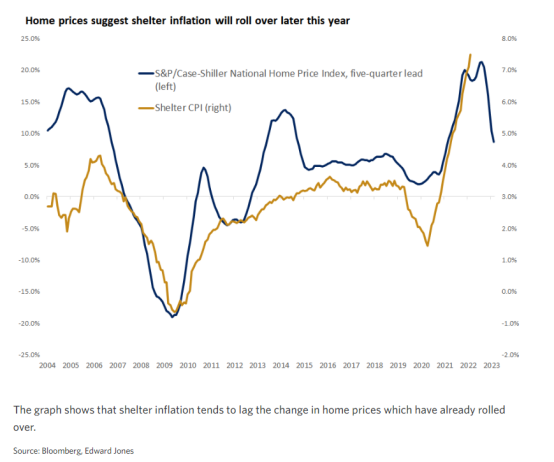

Services inflation ticked higher, as shelter, the biggest component of inflation (accounting for about a third of the overall index), increased the most in three months.

Analysis

Investors have gained more confidence that the inflation tide is receding, helping sentiment stabilize. But as inflation data now match expectations, markets might need some further fuel to continue to march higher. That dynamic was evident in the muted reaction from stocks following the CPI release. As the year progresses, the focus is likely to shift from inflation to growth.

Recent economic data have stayed resilient, though the Fed’s aggressive rate hikes will likely hit the economy with the lag. That is the message from leading economic indicators, such as the inverted yield curve and the decline of manufacturers’ new orders.

With activity likely softening in the months ahead, corporate earnings could come under pressure and be an instigator of volatility. Investors got a small taste of that, as U.S. banks kicked off the fourth-quarter reporting season last Friday. For the quarter, analysts expect earnings for the S&P 500 to have declined 4% from a year ago, the first decline since the third quarter of 20202. The silver lining is that any earnings weakness may already be priced into the market, reflected in the out-sized decline in valuations last year.

Lastly, a recent string of better news from abroad argues against the potential of a deep global recession. Mild weather has helped avert the energy crisis in Europe this winter, resulting in softer inflation and better-than-expected economic data. In response, European equities have gained about 6% halfway through January, the best start to a year on record for the region, and outperforming the U.S. market since September 1. At the same time, prospects for China’s growth have brightened, thanks to the expected economic reopening as the country pivoted away from its zero-COVID-19 policy, while measures have been announced to support the property market. -EJ

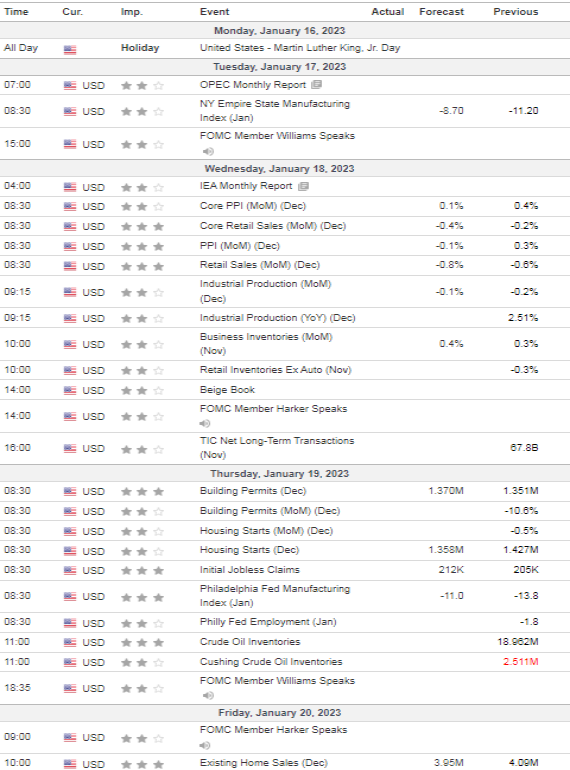

MARKET MOVERS THIS WEEK

Another slow week, most attributed to the US MLK holiday on Monday

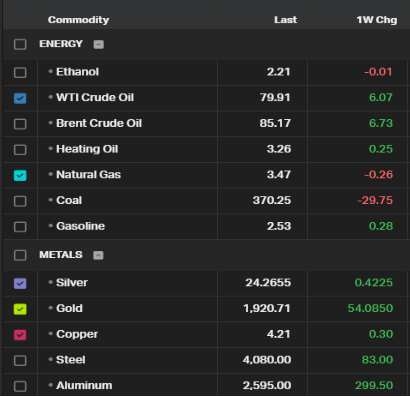

COMMODITIES PERFORMANCE

Month to Date Commodities Performance

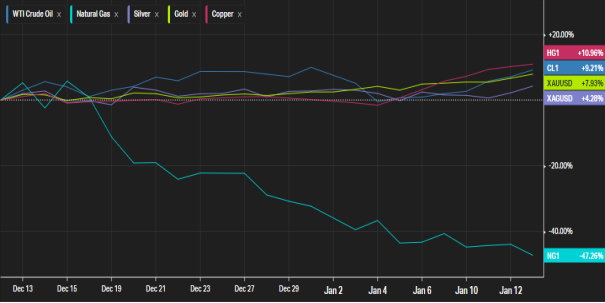

Week to Date Commodities Performance

LOOKING AHEAD TO THIS WEEK-TECHNICALS

$DXY

No explanation needed

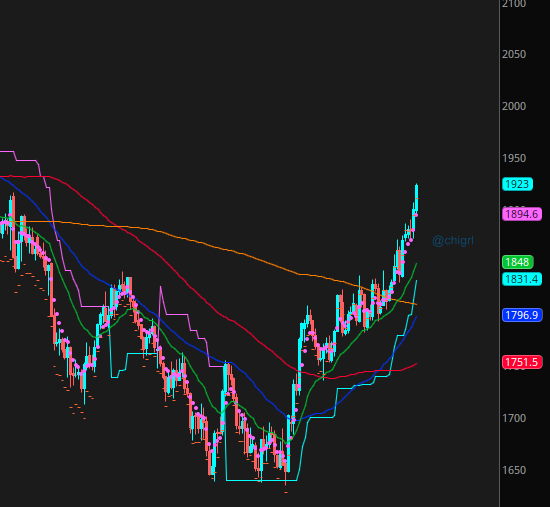

GOLD: Gold is breaking out, and has now caught up with silver in the fact that it is well above the 200 day. We are very overbought, a pullback next week would be welcome to see this market mover higher. The chart is bullish.

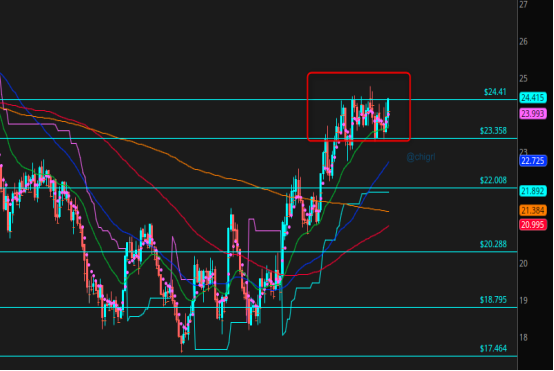

SILVER: silver continues to consolidate for another week. This move will be explosive ..what ever direction it takes. Love straddles for this week. That said, I lean toward the upside in this market.

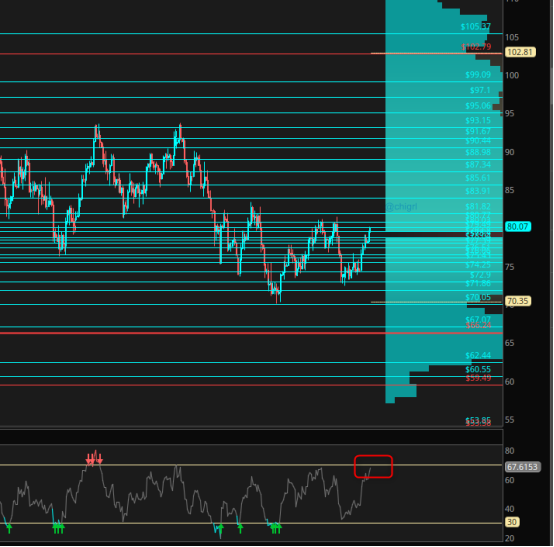

COPPER: Last week I noted ” this market has made number attempts at $3.9 ….any positive news in China will send this contract on a short squeeze” We got our squeeze! Looking forward to next week, we may see some consolidation before moving higher.

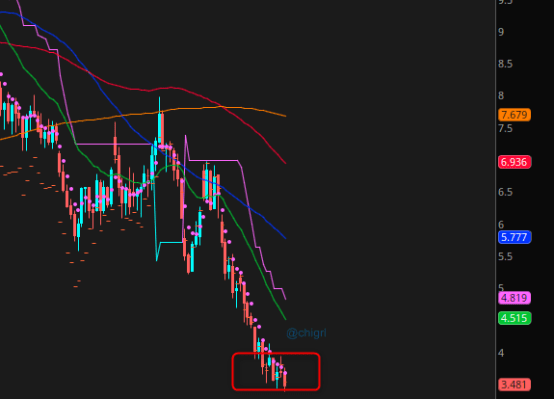

NATURAL GAS: No change. For the last month, I have been saying this chart is very bearish. We are hitting some sort of support and this market is very oversold. That said, I think we consolidate down here for another week or two before the cold front moves into Europe and/or Freeport actually re-opens. If neither one of these scenarios take place, the path of least resistance is down.

Crude Oil: I mentioned last week that we were oversold and this market has staged a comeback. That said, I still believe this market will remain volatile intraday at least until the Chinese Lunar New “Year is over. We are getting a bit overbought..keep in mind. Again, this week could be volatile.

Financial Disclaimer: This material has no regard for specific investment objectives, financial situations, or particular needs of any user. This material is presented solely for informational and entertainment purposes and is not to be construed as a recommendation, solicitation, or an offer to buy or sell / long or short any securities, commodities, or any related financial instruments. Nor should any of its content be taken as investment advice. The views expressed here are completely speculative opinions and do not guarantee any specific result or profit. Trading and investing are extremely high risk and can result in the loss of all of your capital. Any opinions expressed here are subject to change without notice. We may have an interest in the securities, commodities, and/or derivatives of any entities referred to in this material. We accept no liability whatsoever for any loss or damage of any kind arising out of the use of all or any part of this material. We recommend that you consult with a licensed and qualified professional before making any investment or trading decisions.